If you are a Big Three retiree from Ford, GM, or Stellantis and you have a lump sum option on your pension, one hidden factor has an outsized impact on what you walk away with.

Interest rates.

Choosing between keeping the monthly pension and taking the lump sum is not just about preference. It is driven by how your future pension checks are converted into one number today using interest rates and time value of money math.

For many retirees, that "invisible math" is not a technical footnote—it can change the offer by six figures.

That became painfully clear in 2022. In a matter of months, the Federal Reserve raised short-term interest rates from near 0% to over 4%, and long-term corporate bond yields moved sharply higher as well.

When that happened, lump sum values for many autoworkers dropped quickly, even though the underlying pension formulas and years of service did not change at all.

Pension lump sums are calculated by taking all your future monthly payments and "discounting" them back to today using interest rates set by the IRS, called segment rates, which are tied to corporate bond yields. When those rates go up, the present value of the same stream of payments goes down.

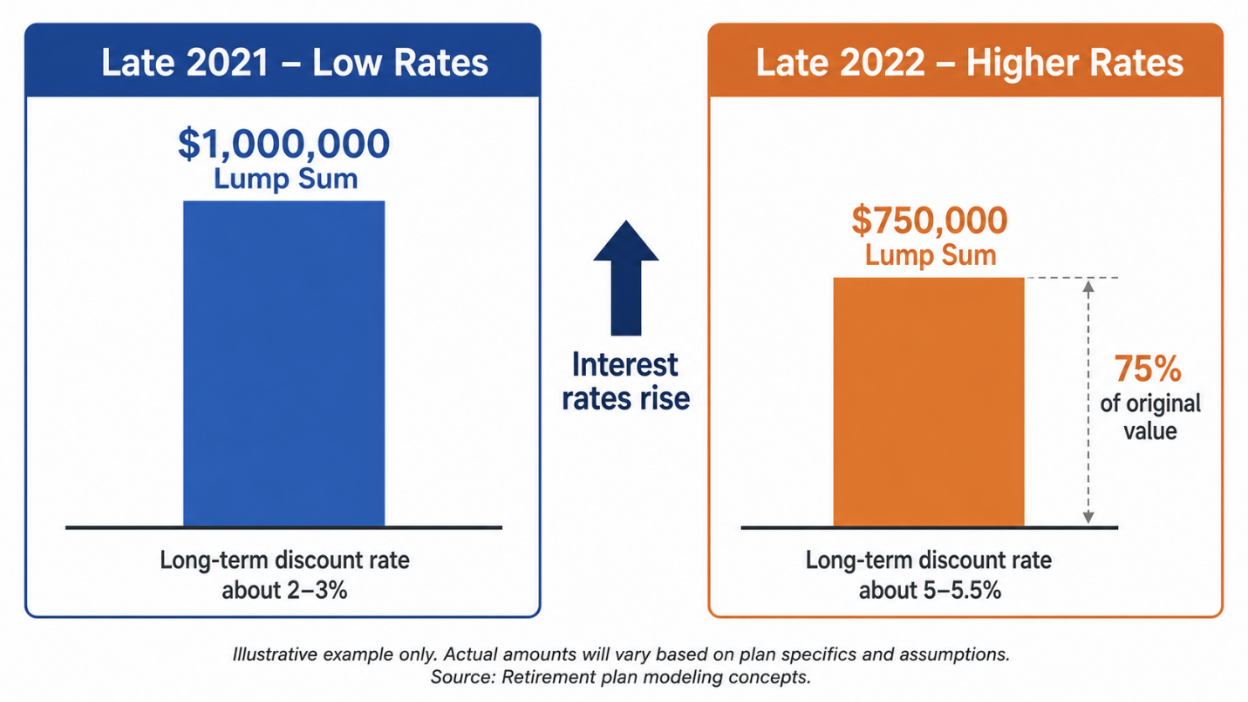

For many Big Three participants, that meant seeing their lump sum offers fall by 20% to 30% in a single year. A $1,000,000 lump sum in late 2021 could have turned into about $750,000 by late 2022—without you doing anything differently.

Illustrative example only. Actual amounts will vary based on plan specifics and assumptions.

That is hundreds of thousands of dollars gone, purely because the interest rates in the formula changed. This is the part most people do not see coming.

Why It Works This Way

A lump sum is simply the present value of future monthly payments.

- Lower interest rates → higher lump sum

- Higher interest rates → lower lump sum

Most plans use three IRS segment rates based on different time horizons. Because pension payments stretch over decades, long-term rates matter the most.

That's especially important for younger retirees with longer payout timelines.

A Special Note for Stellantis Retirees

If you're at Stellantis (formerly Chrysler/FCA), your situation is different.

Lump sums are typically only available during specific windows, and those windows are controlled by the company.

By the time the paperwork hits your desk, the decision is often already partially made for you by interest rate levels.

Where We Are Now—And Why Rate Cuts Don't Fix It

The Fed has started cutting rates again, and many people assume that means lump sums will rebound.

Unfortunately, it's not that simple.

The Fed controls short-term rates.

But lump sums are driven mostly by long-term rates, which depend on:

- Inflation expectations

- Government debt levels (i.e. treasury issuance)

- Bond market demand

- Broader economic outlook

This relationship becomes evident when you look at how 10-year and 30-year government bond yields behaved even after the Fed cut rates for 2 years in 2024 and 2025.

Source: Koyfin. Shows how long-term rates stayed elevated despite Fed rate cuts.

The Fed Funds rate went from 5.5% to 3.75% but long-term rates actually increased slightly. If you were holding out for a recovery in the lump sum value, it hasn't happened yet.

What This Means for You

Here is how all of this plays into your actual retirement decision:

- Your lump sum is not a fixed number. It can move up or down from year to year based on interest rates, even if your pay and service do not change.

- Timing matters more than most people realize. Two people with identical careers can see very different offers simply because they retire in different rate environments.

- Your plan's rules still set the boundaries. Lookback months, stability periods, and (for Stellantis) limited windows all affect when rate changes actually hit your lump sum.

- Building a plan around "rates going back to 2021" is risky. You can hope for that outcome, but you cannot count on it.

For most Big Three retirees, that means the right move is not to chase a perfect rate environment, but to understand how your specific plan works and how much risk you want to take with the lump sum once you have it.

The Bottom Line

Interest rates aren't just background noise. They're often the single biggest factor in what your pension is worth the day you retire. And in some cases:

Timing alone can change the outcome by hundreds of thousands.

If you are within a few years of retirement, it is worth running the numbers on your specific pension—how your lump sum is calculated, how sensitive it is to rates, and how it fits with your other savings—before you make an irreversible choice. That is the kind of analysis we do every day for Big Three retirees in Southeast Michigan.